How I Mastered Startup Capital Without Losing Sleep

Every founder knows the panic of watching cash burn while chasing dreams. I’ve been there—staring at spreadsheets, wondering if my idea was worth the risk. What changed? Not luck, but skills. Real financial know-how transformed how I raised, managed, and multiplied startup capital. This isn’t theory; it’s what saved my business. Let me show you the mindset and moves that made the difference—no jargon, just truth. The journey from uncertainty to control wasn’t easy, but it was necessary. Behind every successful startup is not just a great idea, but a founder who learned to speak the language of money before running out of time.

The Reality Check: Facing the Capital Gap

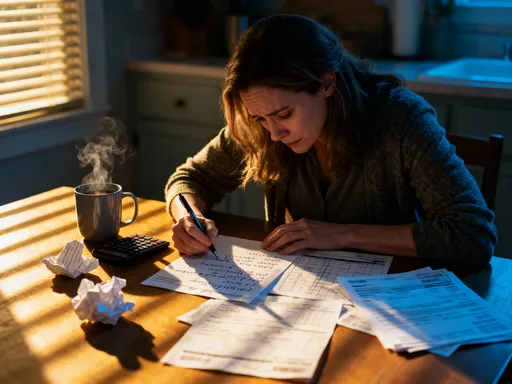

Many entrepreneurs begin with passion, vision, and a prototype. Few begin with a solid grasp of financial reality. The gap between inspiration and funding is where most startups stumble. It’s not uncommon for founders to pour personal savings into their ventures, believing early traction will naturally lead to investment. But when customer growth slows, expenses rise, and investor interest remains lukewarm, the emotional toll intensifies. Sleepless nights become routine. Doubt creeps in. Is this dream sustainable, or is it slipping away?

This moment of reckoning is not a sign of failure—it’s an opportunity for transformation. The truth is, capital is not just fuel for growth; it’s a finite resource that must be managed with precision. Founders who treat money as an afterthought often face painful consequences: layoffs, stalled development, or complete shutdown. Financial literacy is not a secondary skill for entrepreneurs—it is foundational. Understanding how much runway you have, where every dollar goes, and when to pivot can mean the difference between survival and collapse.

Consider the story of a founder who launched a sustainable home goods brand. She invested $80,000 of her own savings, secured a small e-commerce platform, and gained early customer traction. But within nine months, her funds were nearly depleted. She had not accounted for shipping delays, inventory overstock, or the cost of customer acquisition. Her sales looked promising on paper, but cash flow was inconsistent. It wasn’t until she sat down with a financial mentor that she realized she had been measuring success by revenue alone—not liquidity. That shift in perspective saved her business. She began treating capital as a tool to be mastered, not a lifeline to be exhausted.

The first step in mastering startup capital is accepting that financial pressure is part of the journey. The goal is not to eliminate stress, but to build systems that reduce uncertainty. This means moving beyond optimism and embracing realism. It means creating a clear picture of your financial position—assets, liabilities, burn rate, and projected milestones. When you face the capital gap with eyes open, you gain the power to act strategically, not react emotionally.

Building Financial Fluency Before the Pitch

No investor funds a dream without data. They fund confidence—confidence that the founder understands the business model, the market, and, most importantly, the numbers. Yet, many entrepreneurs walk into pitch meetings unable to explain their unit economics, gross margins, or customer lifetime value. This lack of financial fluency undermines credibility, no matter how innovative the idea.

Financial fluency doesn’t require an MBA. It starts with mastering a few core concepts. Cash flow forecasting, for example, allows founders to project income and expenses over time, identifying potential shortfalls before they occur. Burn rate—the speed at which a company spends money—helps determine how long the business can operate before needing more funding. Valuation basics help founders understand how much equity they are giving up and whether the trade-off is worth it. These are not abstract ideas; they are practical tools that shape decision-making.

Take the case of a woman launching an online language-learning platform. Her product was well-designed, and early user feedback was positive. But her first two investor meetings ended in silence. She couldn’t answer basic questions: How much does it cost to acquire a customer? What is the retention rate after three months? How much revenue does each user generate over time? After working with a financial advisor, she built a simple dashboard tracking key metrics. When she pitched again, her answers were clear, concise, and backed by data. One investor later said, “I didn’t just believe in your product—I believed in your ability to run a business.” She secured $250,000 in seed funding.

The lesson is clear: knowing your numbers builds trust. It shows investors that you are not just passionate, but prepared. It also strengthens your own decision-making. When you understand the financial mechanics of your business, you can spot inefficiencies, optimize pricing, and allocate resources wisely. Financial fluency isn’t about perfection—it’s about credibility. And credibility opens doors.

Smart Raising: Beyond the Hype of Funding Rounds

Raising capital is often portrayed as a high-stakes race to secure the largest possible round from the most prestigious investors. But chasing big names and big checks can come at a steep cost. Founders may sacrifice too much equity, lose control over strategic decisions, or become dependent on continuous funding to survive. The smarter approach is to raise with intention—choosing funding sources that align with your vision, timeline, and values.

Bootstrapping, for example, allows founders to retain full ownership and move at their own pace. While it requires discipline and often slower growth, it builds resilience. One tech founder bootstrapped his SaaS company for two years, reinvesting early revenue into product development. By the time he sought external funding, he had a proven model, steady customers, and leverage in negotiations. He raised $1 million at a favorable valuation—without giving up majority control.

Angel investors offer another viable path. Unlike venture capitalists, many angels bring not just capital but mentorship and industry connections. A food entrepreneur raised $150,000 from a network of local angel investors who believed in her mission to support organic farming. These investors were patient, offered guidance, and didn’t pressure her to scale prematurely. Their support allowed her to grow sustainably, opening two storefronts within three years.

Revenue-based financing is gaining popularity as a flexible alternative. Instead of giving up equity, founders repay investors a percentage of future revenue until a predetermined cap is reached. This model aligns incentives—investors succeed only if the business grows. A fitness app founder used this method to raise $200,000, avoiding dilution while maintaining control. His monthly repayments adjusted with revenue, reducing pressure during slower months.

The key to smart raising is asking the right questions: What level of control am I willing to give up? Do these investors understand my long-term vision? Are their expectations realistic? Fast money often comes with hidden costs—pressure to scale too quickly, demands for aggressive growth, or misaligned priorities. Choosing investors who share your values and timeline can be more valuable than the largest check.

Stretching Every Dollar: Operational Discipline That Scales

Once funding is secured, the real test begins: how to make it last. Many startups fail not because they lack ideas, but because they lack discipline. The arrival of capital can create a false sense of security, leading to premature hiring, expensive office spaces, or unnecessary features. But operational efficiency isn’t about cutting corners—it’s about maximizing value from every dollar spent.

One of the most effective strategies is lean operations. This means focusing on core activities that directly drive growth and outsourcing or delaying the rest. A software startup, for example, delayed hiring full-time developers by partnering with a freelance engineering team. This reduced payroll costs by 60% in the first year while maintaining product quality. They used the savings to invest in customer support and onboarding—areas that directly impacted retention.

Zero-based budgeting is another powerful tool. Instead of basing next month’s budget on last month’s spending, every expense must be justified from scratch. A beauty brand applied this method and discovered they were overspending on sample packaging by 35%. By renegotiating with suppliers and simplifying design, they redirected those funds into digital advertising, increasing customer acquisition by 22%.

Milestone-driven funding ensures that capital is released in stages, tied to specific goals such as user growth, revenue targets, or product launches. This creates accountability and reduces waste. A founder of an eco-friendly cleaning product line structured her $300,000 raise into three tranches: $100,000 for prototype development, $100,000 for initial production, and $100,000 for marketing and distribution. Each tranche was unlocked only after meeting predefined metrics. This approach kept spending focused and minimized risk.

Operational discipline scales with the business. The habits formed in the early stages—careful spending, constant evaluation, and strategic prioritization—become the foundation for sustainable growth. Founders who master this phase don’t just survive; they build businesses that can thrive with or without external funding.

Risk Control: Protecting Your Runway Like Your Business Depends On It (Because It Does)

Startups are inherently risky, but not all risks are equal. Some are strategic and necessary; others are avoidable and catastrophic. The difference lies in awareness. Financial blind spots—such as overhiring, premature scaling, or misaligned burn rates—are among the most common causes of startup failure. The good news is that most of these risks can be anticipated and managed with the right systems in place.

Overhiring is a classic mistake. Excitement over funding can lead founders to hire too many people too soon, often in roles that aren’t immediately critical. Salaries and benefits quickly consume cash, and if revenue doesn’t keep pace, layoffs become inevitable. A better approach is to hire for gaps, not aspirations. Focus on roles that directly impact revenue, product development, or customer experience. Use freelancers or part-time staff for secondary functions until growth justifies full-time hires.

Premature scaling—expanding operations before achieving product-market fit—is another silent killer. Launching in new markets, adding features, or increasing production without validated demand can drain resources fast. A beverage startup launched nationwide distribution after a successful local launch, only to find that regional preferences varied widely. Unsold inventory piled up, and cash flow dried up. Had they tested one new market at a time, they could have adjusted their strategy without financial ruin.

Monitoring financial early warnings is essential. Slowing customer acquisition, rising customer acquisition cost (CAC), declining retention, or increasing burn rate are all red flags. Founders should set up dashboards to track these metrics weekly. When CAC rises, it may signal that marketing channels are saturated. When retention drops, it could indicate product issues. These signals allow for early intervention—adjusting pricing, refining messaging, or improving onboarding—before the problem escalates.

Creating buffers and contingency plans adds another layer of protection. This could mean keeping three to six months of operating expenses in reserve, securing a line of credit before it’s needed, or identifying cost-cutting measures that can be implemented quickly. The goal is not to avoid risk entirely, but to ensure the business can withstand setbacks without collapsing.

Cash Flow Is King: Managing Liquidity with Precision

Revenue is a measure of success. Profit is a measure of efficiency. But cash is what keeps the lights on. Too many founders confuse revenue with available funds, only to realize too late that their money is tied up in unpaid invoices or slow-moving inventory. A business can be profitable on paper and still run out of cash—this is why liquidity management is non-negotiable.

One of the most effective ways to improve cash flow is to tighten receivables. This means invoicing promptly, offering early payment discounts, and following up on overdue accounts. A B2B services founder reduced her average collection time from 60 to 28 days by implementing automated reminders and requiring 50% upfront for new clients. That change added four months to her runway without increasing sales.

Negotiating payment terms with suppliers can also make a significant difference. Extending payables from 30 to 60 days gives businesses more breathing room. A manufacturing startup negotiated net-60 terms with three key suppliers, freeing up $75,000 in working capital during a critical product launch phase. In return, they committed to larger, more consistent orders—creating a win-win.

Short-term liquidity tools, such as invoice financing or business lines of credit, can provide temporary relief during cash crunches. However, these should be used strategically, not as a permanent fix. Interest and fees add up, and dependency on debt can create new risks. The goal is to use these tools to bridge gaps, not mask underlying problems.

Ultimately, cash flow management is about timing. It’s about ensuring that money comes in before it needs to go out. Founders who master this skill gain flexibility—whether it’s seizing an unexpected opportunity, weathering a market dip, or investing in innovation. Cash flow isn’t just a number; it’s a source of freedom.

From Survival to Strategy: Using Financial Skills to Scale Confidently

When a startup moves from survival mode to stability, the focus shifts from reacting to planning. Founders who have mastered financial discipline are no longer driven by fear—they are guided by data. This transition is transformative. It allows for strategic expansion, not desperate growth. It means entering new markets, hiring key leaders, or launching new products with confidence, not hope.

Strong financial habits enable smarter decision-making. Instead of guessing which marketing channel works best, founders can analyze return on ad spend (ROAS) and allocate budgets accordingly. Instead of hiring based on gut feeling, they can assess team capacity and projected workload. Instead of launching products based on assumptions, they can run pilot programs and measure unit economics before scaling.

Aligning financial metrics with strategic goals ensures that growth is sustainable. For example, a founder planning to expand internationally can model the costs, forecast local demand, and set milestones for break-even. This reduces risk and increases the likelihood of success. Data becomes the compass, not the rearview mirror.

Financial skill is not about spreadsheets or complex models. It’s about clarity, control, and confidence. It’s about knowing that you can adapt, pivot, or grow—because you understand the mechanics of your business. It’s about sleeping better, not because the risks are gone, but because you’re prepared for them.

Mastering startup capital isn’t a one-time achievement. It’s an ongoing practice. It requires discipline, curiosity, and the willingness to learn. But for those who commit to it, the reward is more than financial stability—it’s the freedom to build something meaningful, lasting, and truly their own.